What if your new manufacturing facility could generate nearly $1 million in first-year tax deductions, enough to fund new equipment and hire additional staff? This isn't theoretical. It's what we delivered for a client who had just completed construction on a 120,000-square-foot facility with warehousing, production space, and an office build-out after reclassifying over $3 million in assets through cost segregation.

Stories like this are common in industrial real estate. Manufacturing plants, warehouses, and distribution centers are loaded with fast-depreciating assets, equipment pads, specialized electrical systems, HVAC components, loading docks, and site improvements. But unless you break them out properly, the IRS treats everything like a 39-year building, even components that clearly don't last that long.

Here's what matters: The IRS allows you to reclassify these components into 5-, 7-, or 15-year depreciation categories. Instead of waiting decades to recover your investment, you can claim substantial deductions immediately.

R.E. Cost Seg specializes in working with manufacturers, warehouse owners, and logistics developers to uncover the hidden value in every property. Our engineering-based studies typically reclassify 30% to 45% of an industrial property's depreciable basis into shorter-life categories, generating six-figure to seven-figure tax savings in year one.

This article breaks down exactly which industrial property components qualify for accelerated depreciation and what it means for your bottom line.

What Cost Segregation Means for Industrial Property Owners

If you own or operate industrial real estate, like a warehouse, manufacturing plant, cold storage facility, or distribution center, chances are you're sitting on a tax asset that hasn't been properly unlocked.

Here's what you need to understand about how cost segregation works in plain terms:

1. Most Industrial Properties Are Depreciated Too Slowly

When you buy or build a property, the IRS lets you write off that cost over time. For industrial buildings, the default depreciation schedule is 39 years. That means you deduct just a small slice of the cost every year, even though many parts of that building won't last anywhere near that long.

In reality, a large share of your building isn't part of the permanent structure at all. It includes components like racking, specialty lighting, reinforced concrete for loading areas, dedicated HVAC systems for manufacturing, and exterior site work, all of which wear out or become obsolete far sooner.

2. Cost Segregation Identifies and Reclassifies These Components

Cost segregation is the process of identifying all the parts of your property that can legally be treated as short-life assets, meaning they can be depreciated over 5, 7, or 15 years instead of 39.

Here's how that typically looks in an industrial facility:

- 5-Year Property: Equipment foundations, electrical for machinery, specialty lighting, data cabling, racking systems.

- 7-Year Property: Office furniture, lockers, and some internal-use equipment.

- 15-Year Property: Paving, loading docks, fencing, drainage, exterior lighting, landscaping.

A study dissects the property component by component, then classifies each piece according to IRS guidelines. This isn't done by guessing. It's handled by professionals who combine engineering knowledge with tax law expertise. An engineering-based study with a site visit ensures these components are properly identified and documented for IRS compliance.

3. The Goal: Front-Load Depreciation to Improve Cash Flow

Once those components are identified and reclassified, they become eligible for accelerated depreciation. That means much larger deductions in the early years of owning or improving the property, especially under the current bonus depreciation rules that allow 100% first-year write-offs for qualifying assets acquired and placed in service after January 19, 2025.

The outcome? You reduce taxable income dramatically in year one, which improves cash flow and often reduces your overall tax liability for the first several years of ownership. For industrial property owners with high capital expenditures, this can significantly improve internal rates of return.

One important consideration: accelerated depreciation isn't free money, it's a timing benefit. When you sell the property, depreciation taken on 5- and 7-year personal property is subject to recapture as ordinary income (up to 37%) rather than at the 25% unrecaptured Section 1250 rate that applies to building depreciation. For owners planning a long hold or 1031 exchange, the math still works in your favor.

What Can Be Reclassified? Key Components in Industrial Buildings

Industrial properties vary widely, but they often include high-value components that qualify for accelerated depreciation. A good study typically breaks down:

- Specialized electrical systems Dedicated wiring for machinery, control panels, subpanels, and high-voltage service lines.

- HVAC and ventilation systems Zoned HVAC, dust collection, fume hoods, exhaust fans, and systems serving production (not comfort) space.

- Plumbing for operations Compressed air lines, water lines to equipment, drains in production floors, and washdown stations.

- Concrete pads and equipment foundations Poured-in-place concrete for heavy machinery or exterior storage that's not structural.

- Interior finishes Epoxy floors, insulated wall panels, modular partitions, industrial shelving, and lighting tied to specific production areas.

- Site improvements Paving, fencing, retaining walls, signage, exterior lighting, landscaping, and stormwater systems.

These elements wear out, become obsolete, or are replaced well before the 39-year mark, making them ideal candidates for reclassification under a proper study.

When to Consider a Cost Segregation Study

Timing can make a big difference in how much value you extract from a cost segregation study. Here's when it's most effective:

- After new construction is completed If you've just finished building or expanding your facility, a study can immediately reallocate assets before depreciation begins.

- When purchasing an existing building Even without improvements, the purchase price can be broken down to accelerate portions like site work and utility infrastructure. Keep in mind that land value must be excluded from the depreciable basis, so proper allocation is essential.

- After renovations or equipment-driven upgrades Retrofitted an assembly line, added ventilation, or updated drainage systems? Those improvements likely contain assets eligible for faster depreciation.

- During the planning or budgeting phase Engaging a cost segregation specialist early allows for better tracking of costs, improving accuracy and results.

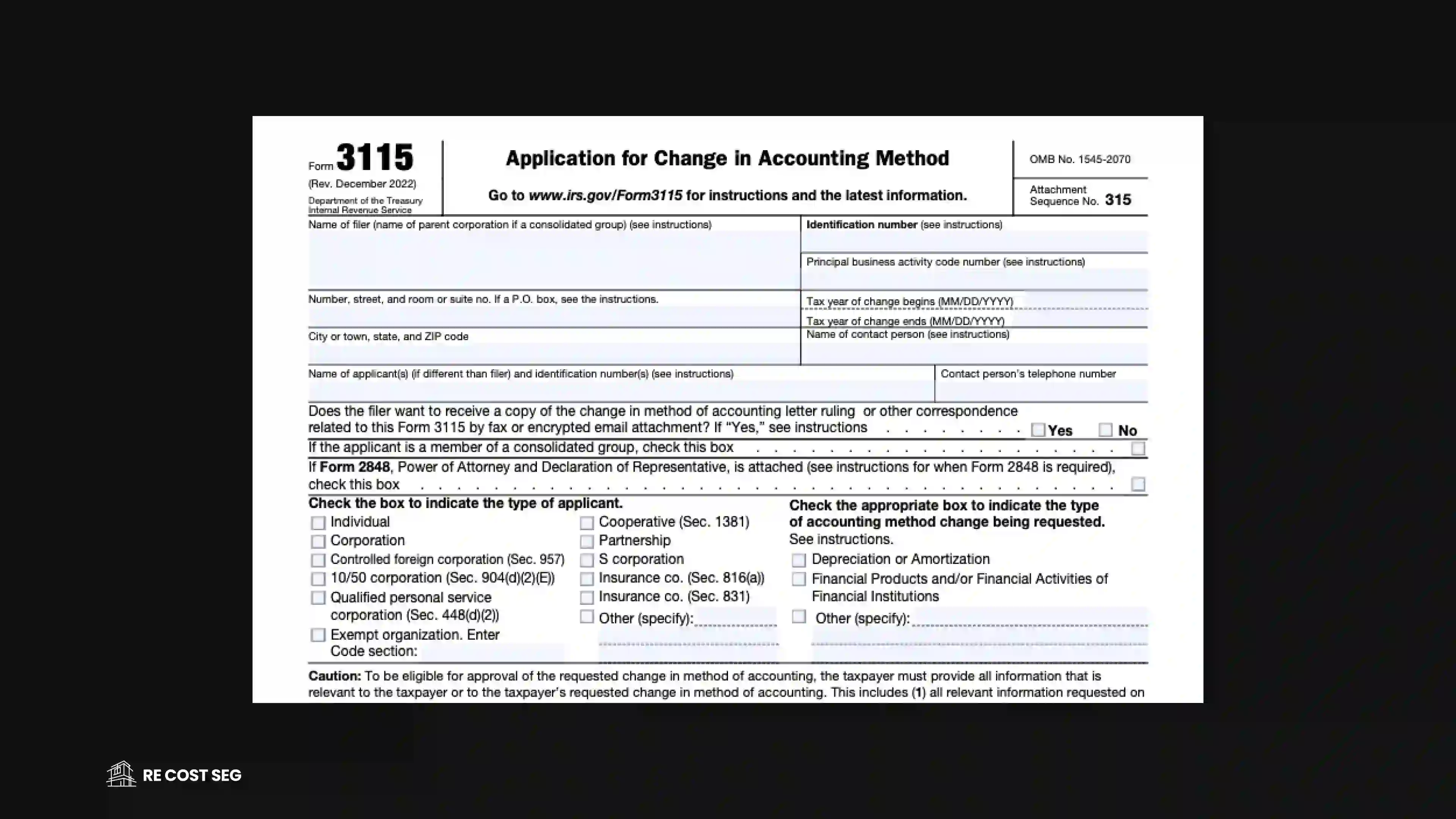

- Even years after you've placed the property in service Through a retroactive study and Form 3115, you can catch up missed depreciation and take the full adjustment in the current tax year—no amended returns required.

Based on my research, here's a new section on Tenant Improvements that you can add to the article. I'd recommend inserting it after the "When to Consider a Cost Segregation Study" section and before the "What are the critical timing rules for 100% Bonus Depreciation?" section, since it deals with a specific scenario that warrants its own callout:

Don't Overlook Tenant Improvements in Industrial Spaces

If you're a landlord building out space for an industrial tenant, or a tenant funding your own improvements, there's a significant cost segregation opportunity that often gets missed.

Industrial tenant improvements (TI) frequently include high-value components like reinforced flooring, specialized electrical systems, climate control for sensitive operations, and production-specific infrastructure. These aren't generic office build-outs. They're engineered for a specific use, and many of those components qualify for accelerated depreciation.

Who Gets to Depreciate Tenant Improvements?

The right to depreciate tenant improvements follows the money, not legal title. Under IRC §168(i)(8), the party who pays for the improvements claims the depreciation, regardless of who manages construction or who owns the improvements at lease termination.

This means:

- Landlord-funded improvements (including tenant improvement allowances): The landlord depreciates, even if the tenant selects contractors and materials.

- Tenant-funded improvements: The tenant depreciates, even if the lease specifies that title transfers to the landlord upon installation.

If you're a landlord offering TI allowances to attract industrial tenants, or a tenant investing in specialized build-outs, a cost segregation study can accelerate those deductions significantly.

Qualified Improvement Property (QIP) Adds Another Layer

Many interior tenant improvements also qualify as Qualified Improvement Property (QIP), which carries a 15-year recovery period and is eligible for bonus depreciation. QIP applies to improvements made to the interior of an existing nonresidential building, as long as the improvement doesn't enlarge the building, involve elevators or escalators, or affect the internal structural framework.

For industrial TI projects, think new production floors, upgraded ventilation systems, or interior partition walls. A cost segregation study can identify which components fall into 5-, 7-, or 15-year categories, and which portions qualify as QIP for bonus treatment.

What are the critical timing rules for 100% Bonus Depreciation?

Understanding the January 19, 2025, Threshold

The One Big Beautiful Bill Act (OBBBA) permanently restored 100% bonus depreciation, but eligibility depends on meeting specific timing requirements. To qualify for the permanent 100% rate, property must be both acquired and placed in service after January 19, 2025.

This distinction matters. Property placed in service between January 1, 2025, and January 19, 2025, as well as property acquired on or before January 19, 2025, and placed in service after that date, remains subject to the prior bonus depreciation phase-down rules, 40% for property placed in service before the end of 2025.

What counts as the acquisition date? Under the regulations, property is not treated as acquired after January 19, 2025, if a written binding contract existed on or before that date. An enforceable contract signed in December 2024 for a facility that won't be completed until mid-2025 means the entire project falls under the 40% rules, not 100%.

The Component Election: A Planning Opportunity for Projects Under Construction

For industrial developers with projects that straddle the January 19, 2025, threshold, IRS Notice 2026-11 confirms that the component election under Section 1.168(k)-2(c) remains available. This election allows taxpayers to claim 100% bonus depreciation on individual components of larger self-constructed assets, even if construction on the overall project began before January 20, 2025.

In practice, this means developers with long lead-time projects can carve out eligible systems, such as special-purpose electrical systems, removable flooring, specialized HVAC, or production equipment foundations, and apply 100% bonus depreciation to those components acquired and installed after January 19, 2025, while the rest of the project depreciates under the 40% rules.

For a manufacturing facility where site work began in October 2024 but interior electrical and HVAC systems weren't installed until March 2025, the component election could recover significant additional deductions on those later-installed systems.

The 10% Safe Harbor for Self-Constructed Property

Industrial owners building their own facilities should understand the 10% safe harbor test. If, before January 20, 2025, you paid or incurred more than 10% of the project's total cost (excluding land and preliminary activities like planning, design, and financing), the project is treated as acquired under the pre-OBBBA rules. The entire eligible basis would generally be limited to 40% bonus depreciation for property placed in service in 2025.

However, even in these situations, the component election provides relief by allowing 100% treatment on qualifying components acquired after the threshold date.

What the Numbers Look Like for an Industrial Project

Imagine you're building a $10 million logistics facility with warehousing, fleet maintenance, and an office mezzanine. After a thorough cost segregation study, roughly 30-45% of the total cost may be reclassified into 5-, 7-, or 15-year property. Let's say $3.5 million.

With 100% bonus depreciation in effect for assets acquired and placed in service after January 19, 2025, that entire $3.5 million could be written off in Year One. That level of accelerated depreciation could result in $800K-$1M or more in tax savings, depending on your tax rate, entity structure, and state tax treatment.

Industrial property owners who qualify for Real Estate Professional Status and materially participate in operations can use these deductions to offset other income directly.

That's money that could go toward upgrading machinery, expanding capacity, or covering operating costs during slower quarters.

Work with a Partner Who Understands Industrial Assets

Industrial buildings are complex, and so is the tax code. Cost segregation helps you align your depreciation schedule with the real-world wear-and-tear of your property's components. But to get the most out of it, you need a specialist who understands both the asset and the strategy.

R.E. Cost Seg works with manufacturers, warehouse owners, and logistics developers to identify eligible assets and deliver results that hold up under scrutiny. We understand the difference between a structural slab and an equipment pad, and we know how to document it properly.

Whether you're breaking ground on a new facility or looking back at prior projects, we'll help you uncover hidden value and reclaim capital you can use today.