Your real estate investments may be hiding thousands of dollars in unclaimed tax deductions. If you've owned commercial or residential rental property for any length of time without conducting a cost segregation study, you're likely overpaying your taxes every year.

The numbers tell the story.

Property owners typically miss 20 to 35 percent of available depreciation deductions when they rely on standard depreciation schedules. For a $2 million property, that translates to $400,000 to $700,000 in accelerated depreciation left on the table.

Look back cost segregation offers a powerful recovery mechanism. Through this IRS-approved process, investors can claim years of missed deductions in a single tax year.

The result? Immediate tax savings that boost current cash flow and improve overall return on investment.

Understanding Look-Back Cost Segregation Studies

What Is a Look-Back Study?

A look-back study is a retroactive cost segregation analysis performed on properties already in service. Unlike contemporaneous studies conducted when properties are first acquired, look-back studies identify and reclassify assets from previous tax years. This reclassification moves components from 27.5 or 39-year depreciation schedules to 5, 7, or 15-year periods.

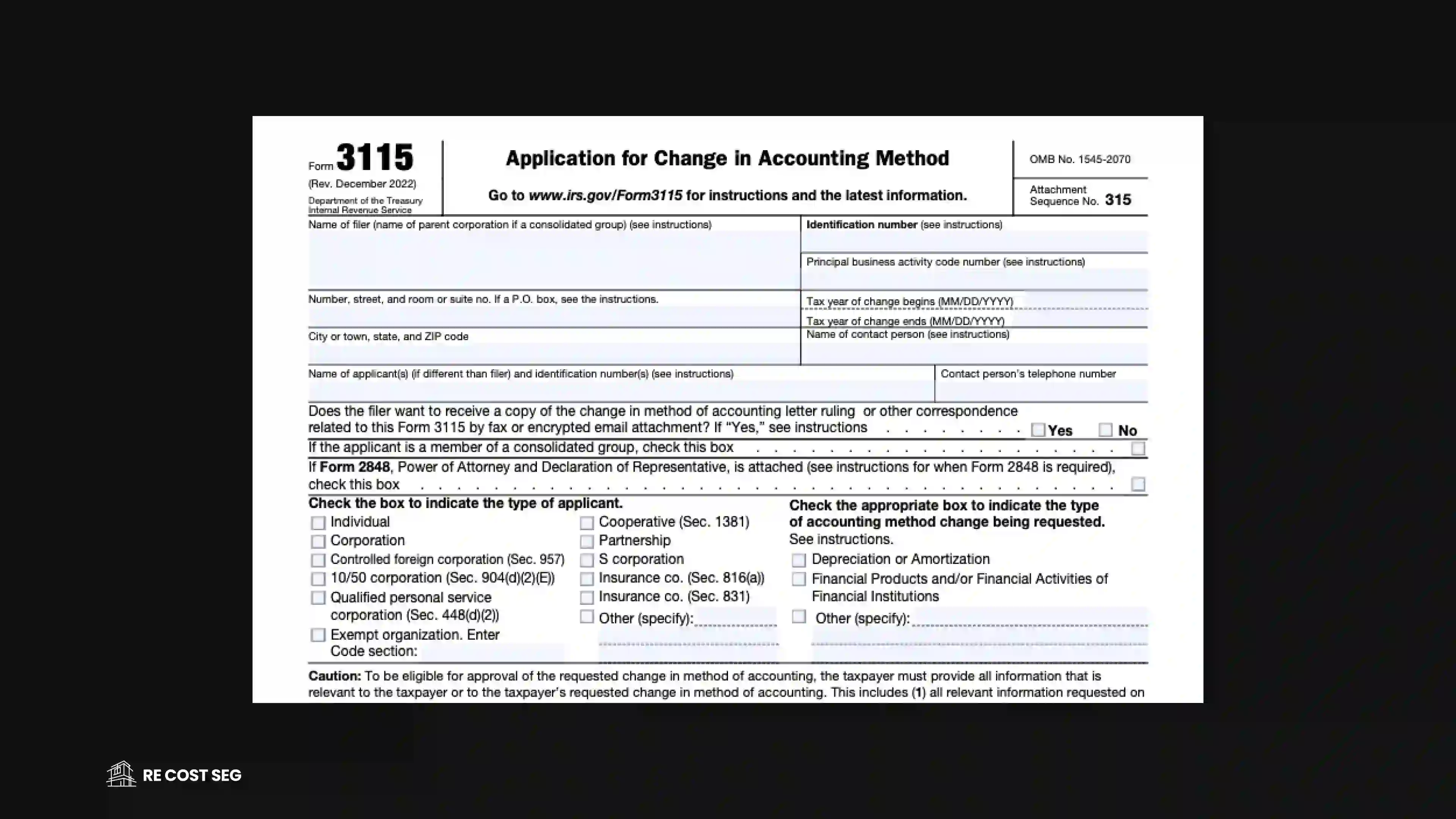

The IRS recognizes this as an accounting method change, not an error correction. This distinction matters. Property owners use Form 3115 to implement the change, capturing all missed depreciation through a Section 481(a) adjustment in the current tax year.

The 10-Year Window of Opportunity

While look-back cost segregation can apply to properties of any age with remaining basis, the greatest benefits typically come from properties placed in service within the past decade. The Section 481(a) adjustment mechanism allows you to claim all previously missed depreciation immediately, regardless of how many years have passed.

Can I really go back and claim depreciation I missed years ago?

Yes. The IRS automatic consent procedures under Revenue Procedure 2015-13 permit taxpayers to change their depreciation method prospectively. You'll file Form 3115 with your current year return, claiming the entire catch-up adjustment without amending prior returns.

The Financial Impact: Real Numbers That Matter

Typical Recovery Scenarios

Consider these actual investor outcomes from retroactive depreciation strategies:

Office Building Example: A $2 million office property purchased five years ago without cost segregation services. The look-back study identifies $600,000 in 5-year property and $300,000 in 15-year property. With standard depreciation already claimed, the Section 481(a) adjustment generates $185,000 in additional first-year depreciation. At a 37% tax rate, this creates $68,450 in immediate tax savings.

Multifamily Property Example: An $5 million apartment complex acquired eight years ago. The study reclassifies $1.5 million into shorter recovery periods. The catch-up depreciation totals $475,000, producing $175,750 in current-year tax savings for an investor at the highest bracket.

The Multiplier Effect

These tax savings create immediate cash flow improvements. That $175,750 from the multifamily example becomes working capital for new acquisitions, property improvements, or debt reduction. The impact compounds when investors reinvest these funds into additional properties with contemporaneous cost segregation studies.

Return on investment calculations shift dramatically. A property yielding 8% annually suddenly delivers an additional 3.5% return in year one through recovered depreciation alone. For real estate professionals with multiple properties, the cumulative effect across a portfolio can reach millions in accelerated deductions.

How much can I typically save with a look-back study?

Properties generally yield 20 to 30 percent of the purchase price in accelerated depreciation. Land value and property type affect these percentages, but most commercial and residential rental properties justify the investment in a professional study.

The Technical Process: Making It Happen

Step 1: Property Qualification Assessment

Not every property warrants a look-back study. Properties that qualify are determined through strategic analysis with your CPA. While some advisors suggest $300,000 to $500,000 as a rule of thumb, R.E. Cost Seg has successfully completed studies on properties of all values when the tax savings meaningfully outweigh the study cost. The decision depends on your specific tax strategy and goals, not property value alone.

Commercial properties, multifamily residences, and special-use facilities often yield the highest returns. Properties with recent renovations or improvements present additional opportunities for retroactive depreciation recovery.

Step 2: The Form 3115 Filing Process

The Form 3115 application changes your accounting method for depreciation. This automatic consent procedure under Revenue Procedure 2015-13 requires no IRS pre-approval. You file the form with your current tax return, claiming the full Section 481(a) adjustment in that year.

The adjustment captures the difference between depreciation claimed and what should have been claimed had cost segregation been applied from the start. This single-year catch-up eliminates the need for multiple amended returns while maintaining full IRS compliance.

Step 3: Documentation Requirements

A defensible look-back study requires comprehensive documentation. R.E. Cost Seg provides engineering-based analyses that include detailed asset classifications, photographic evidence from site visits, and cost allocation methodologies. These reports withstand IRS scrutiny by following the guidelines in the Cost Segregation Audit Technique Guide.

Supporting documents include original purchase agreements, closing statements, improvement records, and architectural plans when available. The more detailed the documentation, the stronger the study's foundation.

Do I need to file amended returns for all the prior years?

No. Form 3115 allows you to claim all missed deductions in the current year through the Section 481(a) adjustment. This streamlined process saves time and professional fees while delivering the same tax benefits.

Step 4: Implementation Timeline

Most studies are completed within 30 to 45 days. Coordination with your tax preparer ensures proper filing and maximizes current-year benefits.

Strategic Considerations for Investors

When Look-Back Studies Make Sense

Look-back cost segregation delivers maximum value in specific scenarios. Properties acquired one to ten years ago without initial studies represent prime candidates. Buildings with substantial improvements or renovations multiply the opportunity, as each upgrade creates additional reclassification potential.

High-basis properties with significant remaining depreciation justify the investment in cost segregation services. A $3 million industrial facility purchased seven years ago likely contains $900,000 in accelerated depreciation opportunities. Properties facing sale may also benefit, as accelerated depreciation reduces current tax liability even with recapture considerations at disposition.

Real estate professional status amplifies these benefits. Those qualifying can offset active income with depreciation losses, unlike passive investors, limited to passive income offsets.

Integration with Overall Tax Strategy

Retroactive depreciation must align with broader tax planning. Investors completing 1031 exchanges need careful coordination, as basis adjustments affect future exchange calculations. The timing of Form 3115 filing impacts when benefits materialize, making year-end planning critical.

Consider the interplay with bonus depreciation. While the Big Beautiful Bill restored permanent 100% bonus depreciation for acquisitions made after 19 January 2025, look-back studies recover benefits from properties that predate current bonus provisions. This creates a dual opportunity: catch up on past missed deductions while positioning for future accelerated depreciation.

What if I'm not a real estate professional - can I still benefit?

Yes. Passive investors can use depreciation to offset rental income and other passive gains. Unused losses carry forward indefinitely, offsetting future passive income or reducing gain upon property sale. The tax savings remain valuable even with passive loss limitations.

Risk Mitigation

Quality matters in cost segregation. IRS-compliant studies from qualified firms like R.E. Cost Seg reduce audit risk. Engineering-based methodologies with detailed documentation provide the substantiation the IRS expects. Cutting corners with estimation-based studies invites scrutiny and potential disallowance of deductions.

Common Misconceptions and Pitfalls

Myth-Busting Section

Myth 1: "It's too late to claim past depreciation"

Reality: Section 481(a) adjustments through Form 3115 allow full recovery of missed depreciation from any prior year. The IRS explicitly permits this accounting method change for properties with remaining basis.

Myth 2: "I'll trigger an audit by filing Form 3115"

Reality: Automatic consent procedures are routine IRS filings. Thousands of taxpayers file Form 3115 annually for depreciation method changes. When supported by professional cost segregation services, these changes follow established IRS guidelines.

Myth 3: "Look-back studies are only for large properties"

Reality: There's no strict property value threshold for cost segregation. While some use $300,000 to $500,000 as a guideline, the real driver is whether tax savings exceed study costs. R.E. Cost Seg has delivered positive returns on properties of various sizes when aligned with the client's strategic tax goals.

The real pitfall lies in poor execution. Taxpayers attempting DIY reclassifications or using estimation-based studies risk IRS challenges. Without proper engineering analysis and site visits, studies lack the technical foundation the IRS requires. Recapture issues also surprise unprepared investors who fail to plan for future property sales.

Will changing my depreciation method raise red flags with the IRS?

When done properly with Form 3115 and supporting documentation from qualified cost segregation professionals, this is an IRS-approved accounting method change. The key is following Revenue Procedure 2015-13 requirements and maintaining comprehensive study documentation.

The Action Plan: Your Next Steps

Start with a systematic portfolio review. Identify properties placed in service within the past decade. Gather purchase documentation, including closing statements, depreciation schedules, and improvement records. Properties with substantial land value require special attention, as land cannot be depreciated.

Remember, property value alone shouldn't be the deciding factor. Even owners of lower-value properties may find cost segregation worthwhile in the right strategic context. Consult with your CPA to determine if the benefits align with your overall tax strategy.

Timing matters. Coordinate with your tax preparer to optimize Form 3115 filing. December year-ends approaching? Act now to capture benefits in the current tax year. The study process requires 30 to 45 days, plus time for your accountant to prepare the filing.

Long-Term Strategy Integration

Make cost segregation standard practice for new acquisitions. With 100% bonus depreciation now permanent, every qualifying purchase deserves evaluation. Establish relationships with qualified providers before acquisitions close.

Annual tax planning should incorporate depreciation strategies. Real estate professionals can maximize benefits across their entire portfolio. Even passive investors benefit from systematic depreciation optimization, creating tax-efficient wealth building over time.

The Recovery Opportunity Awaits

Look back cost segregation represents immediate value recovery for real estate investors. Every year without action means more missed deductions and unnecessary tax payments. The combination of retroactive depreciation recovery and current bonus depreciation provisions creates an unprecedented opportunity.

The window for maximizing these benefits won't remain open indefinitely. Statute of limitations considerations and changing tax laws make timing critical. Properties with significant basis sitting on standard depreciation schedules are leaving money on the table.